Zilch has officially introduced Zilch Up, a transformative product aimed at providing more affordable credit to individuals often sidelined by conventional financial systems. This innovative initiative is set to empower millions of users in the UK to build their financial profiles responsibly and without incurring interest fees.

The launch comes on the heels of a successful trial that saw over 25,000 participants boost their visibility with the major credit reference agencies in the UK. According to Zilch, the impact of Zilch Up could be substantial, addressing the plight of the 5 million people classified as credit invisible in the country. Philip Belamant, the CEO and co-founder of Zilch, emphasized the urgency of the situation, stating, “We need to strengthen the protections for consumers and increase access to interest-free and affordable credit – particularly now when the cost of living continues to hurt.”

Belamant outlined the challenges faced by many in accessing credit, pointing out that for far too long, millions have struggled with limited options due to underdeveloped credit histories. “In a digital finance world, this is causing them the stress and crippling pain of funding unaffordable high-interest costs plus the danger of hard to understand late fees,” he explained. Zilch Up aims to eliminate these obstacles by allowing users to improve their credit scores while engaging in zero-interest borrowing.

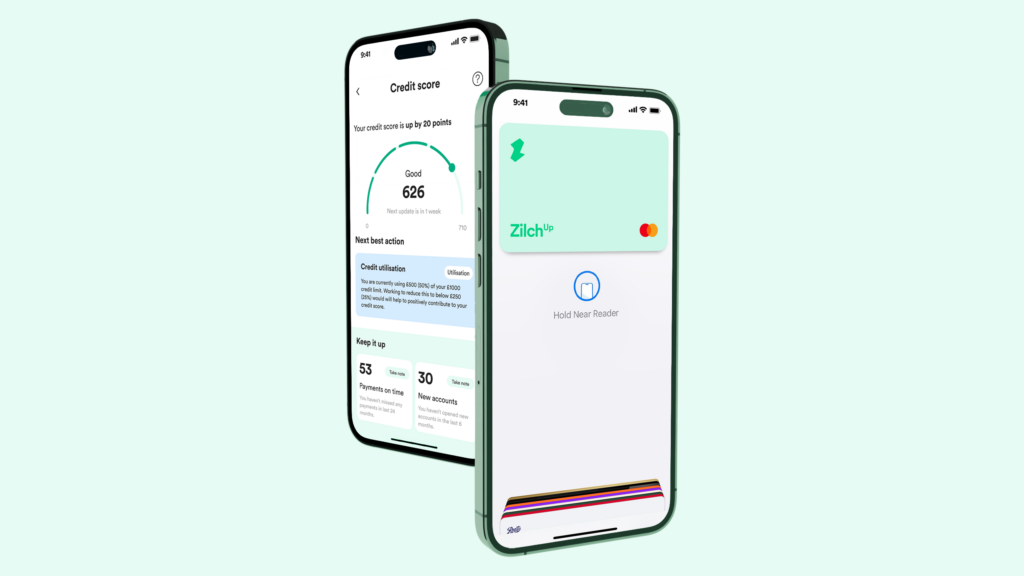

With Zilch Up, customers can enjoy many features of Zilch's classic offerings, including a credit limit starting as low as £50. A distinguishing feature of Zilch Up is the ability for users to pause their credit and utilize the platform as a debit card through the Pay Now option, in addition to earning rewards. Users also have the flexibility to switch to a credit mode, which requires a first payment of just 50% upfront, with the remaining amount due over six weeks.

Moreover, Zilch plans to enrich this offering by introducing personalized credit coaching and enabling users to view their credit scores directly through the Zilch app. “Our new product, Zilch Up, has already lifted over 25,000 customers into mainstream credit, and we intend to help many more,” added Belamant.

Zilch Up embodies a broader commitment to financial inclusivity, representing a significant stride toward establishing a fairer financial ecosystem. By collaborating with leading credit reference agencies, Zilch ensures that consumers can enhance their credit scores through responsible borrowing practices. As a regulated entity in the UK, Zilch assures its users of consumer protections that are often lacking in other forms of borrowing.

By the Numbers

The findings from initial testing highlight that many customers now possess sufficient detail in their credit records to acquire a valid credit history. Unlike traditional high-cost lenders, Zilch offers a pathway for users to build their credit scores by demonstrating responsible borrowing behavior through its innovative structure. Belamant articulated the company’s vision succinctly, stating, “At Zilch, we aren’t waiting. We want to change this status quo by democratising access to interest-free and affordable credit.”

Career Journey

Zilch began its journey from a recognition of the disparities in the accessibility of affordable credit, targeting those at a socioeconomic disadvantage. This mission is evident in its strategic partnerships with major credit agencies, which are crucial for the success of Zilch Up.

As one of the few UK providers of credit via Buy Now, Pay Later (BNPL) systems that report data to consumer credit files, Zilch continues to set a precedent in the sector. Being the first UK homegrown BNPL provider authorized by the FCA, Zilch demonstrates a commitment to ensuring that clients can build their credit ratings safely and effectively.

Looking Ahead

Looking ahead, Zilch's initiative could reshape the financial landscape, providing much-needed access to affordable credit for those who need it most. The introduction of Zilch Up not only expands its user base but potentially changes the way individuals interact with credit systems in the UK.